REG D OFFERING, ACCREDITED INVESTORS ONLY (RULE 506(c))

If You Invested In Real Estate eREITs, Here's The Institutional Upgrade

A real estate operating company (REOC) built to buy, improve, and scale multifamily, with a long-term objective to reach public markets.

GET THE INVESTOR DECK

Operator Equity (REOC)

Own the operating company, not a single-asset deal.

Preferred Structure

Downside-first preference + upside participation (see term sheet).

Liquidity Optionality

Medium/long‑term objective to List on the NYSE American (no guarantee)

Operator Track Record

These results reflect the CEO’s prior real estate projects

Why company-level

real estate has Outperformed

Not a syndication. Not a finite-life fund.

While single buildings are bought and sold based on property-level metrics, real estate operating companies are valued on institutional performance, execution, scale, strategy, and the full portfolio.

Diversified by design

Across multiple acquisitions over time.

Built by operators

Significant Improvements +

hands-on management.

Structured for scale

Process, reporting, and governance.

What this means in practice

Public multifamily operators historically IPO’d at 10–15× earnings multiples (based on reported REIT IPO filings)

Institutional value grows with the company, not one building

Institutions invest in operating companies, not single-asset deals

Operator-level businesses earn higher valuation multiples than individual properties

Why Invest Now

This is a platform story, early capital supports growth, execution capacity, and the ability to add properties over time.

Growing market, lower institutional crowding

Oklahoma and similar secondary markets can be less hyper-competitive than gateway metros.

Scale

Capital supports a stronger team and more properties.

Platform compounding

As properties are added, systems, data, and execution can compound over time.

Operator edge

Heavy renovations and hands-on execution can be less crowded than “clean,” yield-first product.

Location + sourcing

Local focus supports consistent deal sourcing and operational follow-through.

Time leverage

For busy professionals, operator-led execution provides exposure without day-to-day ownership.

The Greenlite advantage

Institutional discipline, operator-led execution, and a focused strategy.

Multi-asset exposure

Own the platform, not just one property.

Value-add focus

Vertically integrated

Sourcing, renovation, and management are operator-led.

Market focus

Concentrated strategy to drive repeatable execution.

Track record

Built from prior acquisitions and realized outcomes.

Long-term liquidity optionality

Medium/long‑term objective to List on the NYSE American (no guarantee)

This is platform equity — not a one-off building and not a finite-life fund — and there are few direct public comps for this strategy. Any future exchange listing is a long-term objective, not a guarantee.

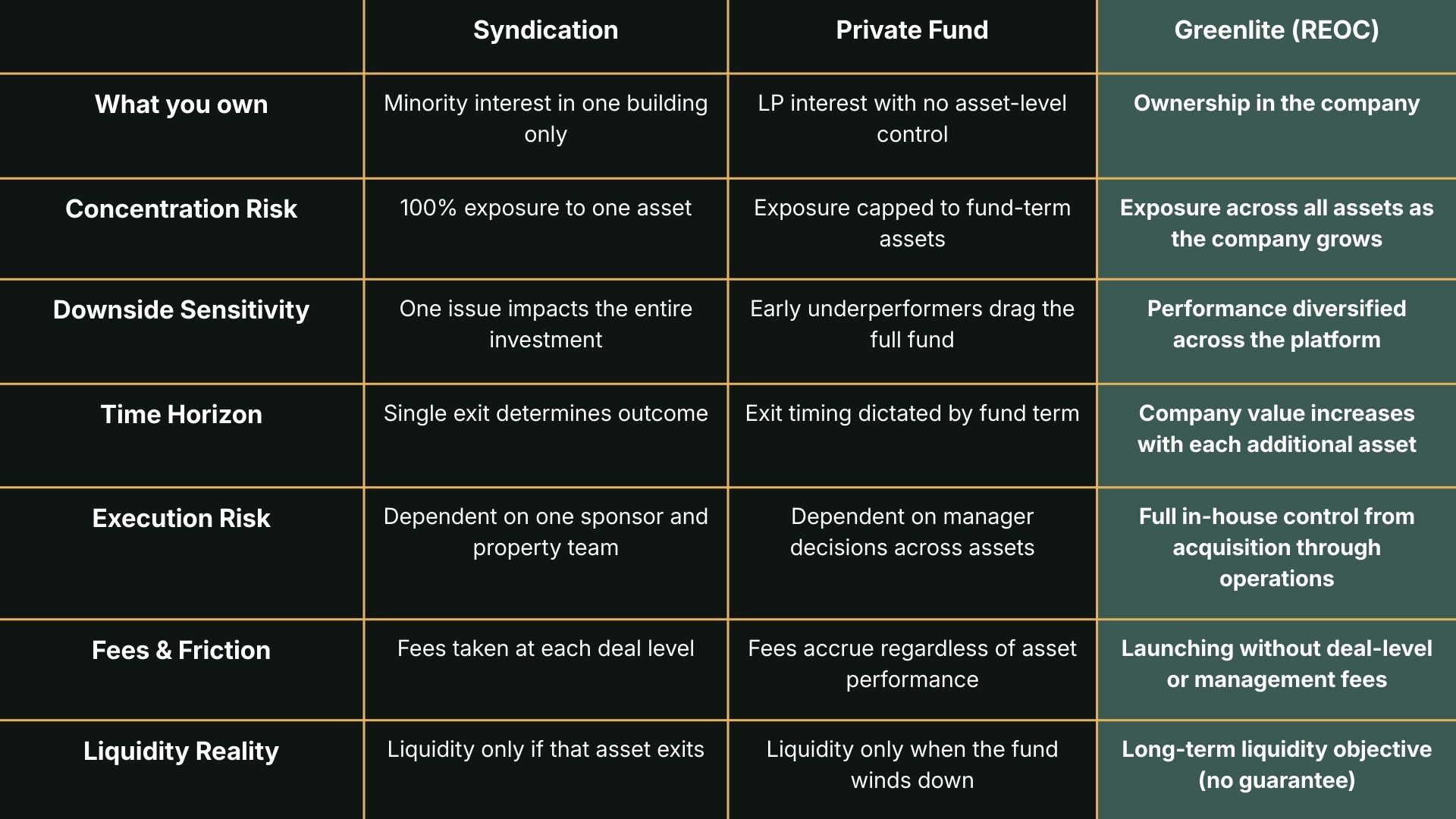

Why Many Accredited Investors Are Looking Beyond Syndications

Syndications can deliver strong outcomes, but the structure has built-in limitations that some investors want to move beyond.

Single-Asset Risk

One deal, one business plan, one outcome.

Deal-by-Deal Fees

Multiple GP fees across separate offerings.

Long Lockups

Capital tied up for 5–7+ years in one property.

Deal Fatigue

Constantly reviewing, selecting, and wiring into new offerings.

No Institutional Upside

Investors participate in the property, not the operator’s long-term growth.

Why Greenlite Holdings Beats eREITs On Fees

Most eREITs layer multiple fees across the investment, acquisition fees, asset-management fees, servicing fees, performance fees, and administrative fees. These stacked charges quietly compound over time and can significantly reduce investor returns.

Greenlite takes a different approach: A simpler, lower-expense structure designed to keep more capital working for investors.

What this means for accredited investors:

Lower all-in expenses compared to typical eREIT fee stacks

No layered charges across acquisition, management, and servicing

More capital deployed into real projects, not administrative overhead

Efficiency from vertical integration, reducing the need for external services

Aligned incentives, performance matters more than fee generation

What you are buying

Not an eREIT product. Series A-1 is structured preferred equity with participation, built for operator-led value-add execution. Management may evaluate institutional liquidity options over time, but no liquidity or listing is guaranteed.

Downside-first

100% preference before common

Upside participation

Participates pro rata after preference

Long-term hold

Multi-year horizon

Platform Equity

vs.

Syndication

vs.

Fund

Three common ways to invest in private real estate, here’s the difference.

Examples from

prior projects

Heavy Renovations

Hands on Execution

Successful Deals

The Restoration on Candlewood

156.71%

ROE

45.89%

IRR

Catalina Vista

179.9%

ROE

47.31%

IRR

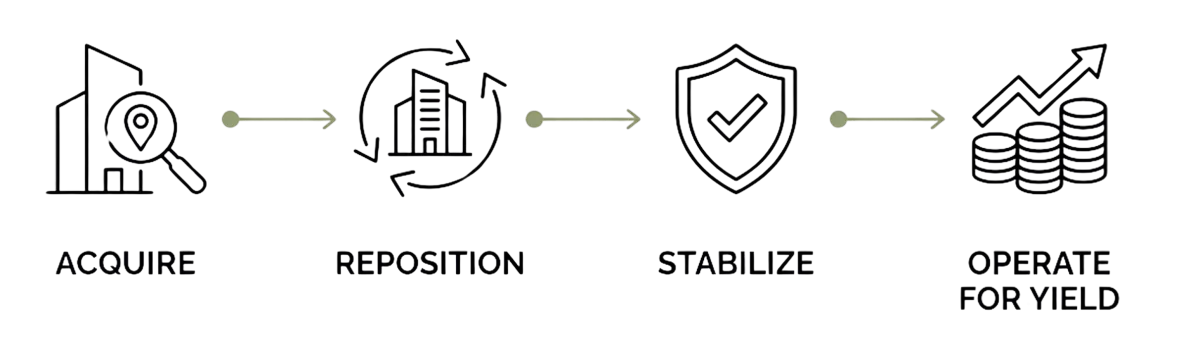

The operating

playbook

Acquire under-performing assets → reposition → stabilize → operate for yield and long-term value.

Medium/long‑term objective to List on the NYSE American (no guarantee)

Long-term, the company’s objective is to evaluate potential liquidity paths — including a NYSE American direct listing — as the platform scales. There’s no guarantee, no timeline, and no promised outcome. But we’re building the reporting, governance, and operating discipline with that direction in mind.

Institutional governance direction

Voting rights and investor protections designed for sophisticated investors (see term sheet).

Reporting discipline

Ongoing effort toward higher standard reporting and audit readiness (see materials for current status).

Strategic liquidity optionality

Management may pursue strategic liquidity paths over time (including potential exchange listing pathways), but no liquidity event is guaranteed.

Frequently Asked Questions

WHAT IS GREENLITE HOLDINGS?

Greenlite Holdings is a Real Estate Operating Company (REOC) that acquires, repositions, and operates Class B/C multifamily and commercial properties. Investors receive company-level equity rather than a stake in a single property.

WHO CAN INVEST UNDER REG D?

This offering is available only to accredited investors as defined by the SEC. Income, net worth, or certain financial credentials must be verified prior to investing.

WHAT IS THE MINIMUM INVESTMENT?

The minimum investment is $10,000.

WHAT AM I INVESTING EXACTLY?

You are investing in equity in the operating company. This provides diversified exposure across multiple assets, consolidated reporting, and participation in company-level outcomes.

HOW MIGHT INVESTORS EARN RETURNS?

Potential returns may come from operational improvements that grow NOI, capital events at the asset level, and long-term company-level outcomes. Returns are not guaranteed.

WHAT TYPES OF PROPERTIES DOES GREENLITE TARGET?

Underperforming Class B/C properties with clear value-add potential—updated interiors, operational improvements, efficiency upgrades, and better management execution.

HOW DOES ESG FACTOR INTO THE STRATEGY?

Greenlite incorporates ESG through energy and water efficiency upgrades, safety improvements, and community-focused enhancements that support long-term occupancy and cost control.

IS THERE A POTENTIAL PATH TO LIQUIDITY?

The long-term objective includes evaluating a direct listing or other company-level liquidity events. No assurance can be given that any specific outcome will occur.

WHAT ARE THE KEY RISKS?

Risks include market conditions, interest rates, operational execution, financing availability, regulatory changes, and other factors. Past performance is not predictive of future results.

HOW DO I REQUEST ACCESS AND REVIEW DOCUMENTS?

Submit the interest form. After accreditation verification, you will receive access to the data room and official offering documents for full review.

HOW IS THIS DIFFERENT FROM AN eREIT OR REIT?

A public REIT/eREIT is typically a pooled vehicle designed for broad investor access and often offers different liquidity mechanics (depending on the product).

Greenlite’s offering is private (Reg D 506(c)), accredited investors only, and you’re buying Series A-1 preferred stock in the operating company (REOC), not shares of a public REIT. Any potential liquidity pathway is a long-term objective, not a guarantee.

HOW LONG IS THE HOLD?

This is a long-term, illiquid investment intended for investors with a multi-year horizon. There is no guaranteed exit date; any potential corporate liquidity event (including a possible listing) is an objective only and not guaranteed.

WHAT FEES EXIST?

Greenlite earns fees for real services performed at the asset level, which may include items like acquisitions, asset management, construction management, and dispositions (if applicable).

Full fee details are provided in the offering materials (PPM/FIM + term sheet + subscription documents).

IS THIS A FUND?

No. This is not a finite-life private real estate fund and not a syndication for a single building.

You are purchasing Series A-1 Voting Preferred Stock in Greenlite Holdings, Inc. (the operating company / REOC).

THE SECURITIES OFFERED HEREBY HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED (THE “ACT”), OR ANY STATE SECURITIES OR BLUE SKY LAWS AND ARE BEING OFFERED AND SOLD IN RELIANCE ON EXEMPTIONS FROM THE REGISTRATION REQUIREMENTS OF THE ACT AND STATE SECURITIES OR BLUE SKY LAWS. ACCORDINGLY, THE SECURITIES CANNOT BE SOLD OR OTHERWISE TRANSFERRED EXCEPT IN COMPLIANCE WITH THE ACT. IN ADDITION, THE SECURITIES CANNOT BE SOLD OR OTHERWISE TRANSFERRED EXCEPT IN COMPLIANCE WITH THE APPLICABLE STATE SECURITIES OR BLUE SKY LAWS. THE SECURITIES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE SEC, ANY STATE SECURITIES COMMISSION OR OTHER REGULATORY AUTHORITY, NOR HAVE ANY OF THE FOREGOING AUTHORITIES PASSED UPON THE MERITS OF THIS OFFERING OR THE ADEQUACY OR ACCURACY OF ANY OTHER MATERIALS OR INFORMATION MADE AVAILABLE TO SUBSCRIBER IN CONNECTION WITH THIS OFFERING. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

THE SECURITIES MAY ONLY BE PURCHASED BY PERSONS WHO ARE “ACCREDITED INVESTORS” (AS THAT TERM IS DEFINED IN SECTION 501 OF REGULATION D PROMULGATED UNDER THE ACT).

THE [OFFERING MATERIALS] MAY CONTAIN FORWARD-LOOKING STATEMENTS AND INFORMATION RELATING TO, AMONG OTHER THINGS, THE COMPANY, ITS BUSINESS PLAN AND STRATEGY, AND ITS INDUSTRY. THESE FORWARD-LOOKING STATEMENTS ARE BASED ON THE BELIEFS OF, ASSUMPTIONS MADE BY, AND INFORMATION CURRENTLY AVAILABLE TO THE COMPANY’S MANAGEMENT. WHEN USED IN THE OFFERING MATERIALS, THE WORDS “ESTIMATE,” “PROJECT,” “BELIEVE,” “ANTICIPATE,” “INTEND,” “EXPECT” AND SIMILAR EXPRESSIONS ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS. THESE STATEMENTS REFLECT MANAGEMENT’S CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS AND UNCERTAINTIES THAT COULD CAUSE THE COMPANY’S ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE CONTAINED IN THE FORWARD-LOOKING STATEMENTS. INVESTORS ARE CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD-LOOKING STATEMENTS, WHICH SPEAK ONLY AS OF THE DATE ON WHICH THEY ARE MADE. THE COMPANY DOES NOT UNDERTAKE ANY OBLIGATION TO REVISE OR UPDATE THESE FORWARD-LOOKING STATEMENTS TO REFLECT EVENTS OR CIRCUMSTANCES AFTER SUCH DATE OR TO REFLECT THE OCCURRENCE OF UNANTICIPATED EVENTS.